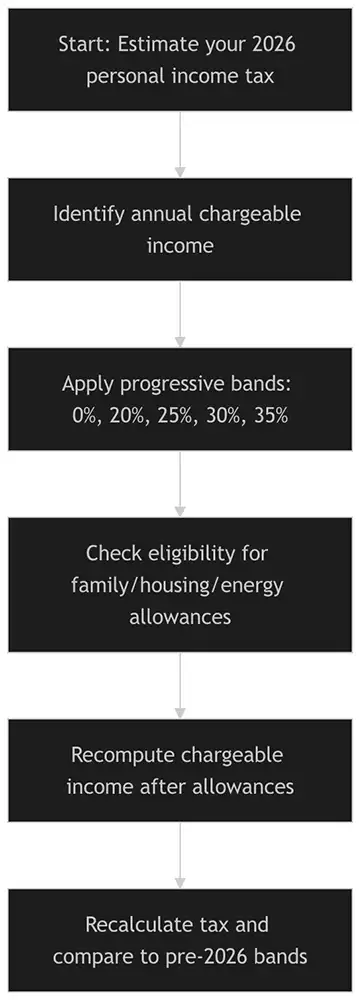

The Cyprus tax reform voted into law in late 2025 is now in force for tax years starting 1 January 2026, and the biggest day‑to‑day impact for most households comes from the updated personal income tax bands.

With Cyprus income tax rates 2026, you get a higher tax‑free threshold and wider mid‑bands, which lowers tax for most chargeable incomes above €22,000—often by several hundred euros a year, and by over €1,500 for higher incomes.

On top of the band changes, income‑tested allowances for children, housing costs, and energy/EV upgrades can reduce taxable income further when you qualify, improving your effective tax rate beyond the brackets alone.

The new 2026 income tax bands in force from 01/01/2026

Cyprus’ comprehensive tax reform was voted into law by the House of Representatives of Cyprus on 22 December 2025 and published in the Government Gazette on 31 December 2025.

The new framework applies for tax years commencing 1 January 2026 and onward, which is why payroll and self‑assessment calculations now use the updated brackets.

Here are the official-style bands as summarized in major professional updates (chargeable income = taxable income after allowable deductions).

Under Cyprus income tax rates 2026, the bands are:

| Chargeable annual income | Marginal rate | Notes |

|---|---|---|

| €0 – €22,000 | 0% | tax-free threshold |

| €22,001 – €32,000 | 20% | first taxable slice |

| €32,001 – €42,000 | 25% | mid-band |

| €42,001 – €72,000 | 30% | wider band vs pre‑2026 |

| Over €72,000 | 35% | top marginal rate begins later |

These updated Cyprus income tax rates 2026 were described as revising thresholds upward in view of household needs and circumstances, signaling a direct “take‑home pay” intention rather than a purely technical adjustment.

What “marginal rate” means in practice

Cyprus personal income tax is progressive: you do not pay 30% on your full income just because you enter the 30% band. You pay each rate only on the slice that falls inside that band.

So, if your chargeable income is €40,000, only the portion above €32,000 is taxed at 25%, not the entire €40,000.

Comparison to the pre‑2026 bands and the “win” you already had

Before 2026, Cyprus already had a meaningful tax‑free band and a relatively simple set of progressive thresholds.

The commonly published pre‑2026 bands (still referenced in 2025 tax summaries) were:

| Chargeable annual income | Marginal rate |

|---|---|

| €0 – €19,500 | 0% |

| €19,501 – €28,000 | 20% |

| €28,001 – €36,300 | 25% |

| €36,301 – €60,000 | 30% |

| Over €60,000 | 35% |

That structure already helped many households keep tax modest at lower incomes, because nothing was due up to €19,500 and only the higher slices faced the higher marginal rates.

Now look at the core shift with Cyprus income tax rates 2026:

- The tax‑free threshold rises from €19,500 to €22,000.

- The top 35% band starts at €72,000 instead of €60,000, meaning a wider slice of upper‑middle income is taxed at 30% rather than 35%.

Assumption used for comparisons below: savings examples treat the “pre‑2026” schedule as the widely published July 2025 bands (PwC Tax Summaries) and the “2026” schedule as the band table shown in the 2026 bill publication updates (PwC) and the 2026 reform analysis (KPMG).

Savings examples and why the change matters

If you want to feel the impact of Cyprus income tax rates 2026 quickly, the best way is to compare tax on the same chargeable income under the two schedules. The table below uses the bracket math exactly as written above.

| Chargeable income | Tax (pre‑2026 bands) | Tax (2026 bands) | Estimated savings |

|---|---|---|---|

| €25,000 | €1,100 | €600 | €500 |

| €30,000 | €2,200 | €1,600 | €600 |

| €40,000 | €4,885 | €4,000 | €885 |

| €60,000 | €10,885 | €9,900 | €985 |

| €80,000 | €17,885 | €16,300 | €1,585 |

| €120,000 | €31,885 | €30,300 | €1,585 |

How to interpret it: once you earn above €72,000 chargeable income, the annual savings stabilize (in these simplified examples) because both schedules apply 35% above the top threshold; the big “rate win” is primarily the widened 30% band and the higher tax‑free threshold.

Beyond the brackets: deductions that can improve your effective rate

Your real outcome under Cyprus income tax rates 2026 depends on what becomes chargeable after deductions and allowances. That’s where the reform’s household‑focused reliefs can matter more than people expect.

The reform introduces income‑tested allowances on a family unit basis, including amounts for dependent children and specific household costs. Eligibility thresholds and amounts are spelled out in the reform analysis, including:

- Dependent child deductions (€1,000 first child, €1,250 second, €1,500 third+; doubled for single‑parent/full custody).

- Housing cost allowances up to €2,000 (interest on a performing loan for purchase/construction of a primary residence in Cyprus, or rent for a primary residence in Cyprus).

- Energy efficiency/green allowances up to €1,000 for specific items (e.g., improvements for a primary residence and certain electric vehicle cases).

This is why many households will feel Cyprus income tax rates 2026 as a “double benefit”: wider tax bands and extra levers to reduce taxable income when you qualify.

Why this matters in real life

For employees, the impact tends to show up as higher net pay (especially in the €25,000–€60,000 band), without needing complex planning—because the bracket structure itself moved in your favor.

For self‑employed professionals and households with children or primary residence costs, the “insurance + housing + family allowance” layer can materially change the final chargeable income, and therefore the effective tax rate you experience under Cyprus income tax rates 2026.

For foreigners planning a move, Cyprus income tax rates 2026 add a practical financial advantage to the island’s lifestyle appeal. When you relocate from a higher-tax country, keeping more of your employment or business income can make a noticeable difference to your monthly cash flow and long-term planning. That is one of the reasons Cyprus continues to attract professionals, entrepreneurs, remote workers, and families who want a better balance between quality of life, tax efficiency, and future stability.

If you want the full picture around the broader 2026 reform (corporate tax, dividend SDC, stamp duty repeal, compliance changes), you’ll find it in Sunshadow’s Cyprus‑wide guides that sit alongside Cyprus income tax rates 2026 coverage.

- Cyprus Taxes 2026 (full reform overview)

- Cyprus Tax Reform 2025 (context and “how we got here”)

- Cyprus Non-Domiciled Status Program (SDC context)

FAQs

Are the 2026 personal income tax bands officially in force now?

Yes. The reform measures were voted into law in December 2025, published in the Official Gazette on 31 December 2025, and apply for tax years commencing 1 January 2026 and onward.

Do these bands apply to your full salary, or to “chargeable income”?

They apply to chargeable income, meaning the taxable amount after allowable deductions and reliefs. That is why allowances (children, housing, insurance) can change the final number that is run through the bands.

What is the biggest single change you’ll notice in 2026?

The tax‑free threshold increases to €22,000, and the 35% top rate starts at €72,000 instead of €60,000, lowering tax for most chargeable incomes above €22,000.

Do dividends, interest, and rent follow the same rules as employment income?

Not always. Personal income tax (PIT) is separate from Special Defence Contribution (SDC), which can apply to certain dividend/interest/rental flows depending on your tax residency and domicile status; some flows can be exempt for non‑doms.

Why do some people see bigger benefits than others under Cyprus income tax rates 2026?

The bracket shift helps most earners mechanically, but the largest percentage improvements usually come when you also qualify for the income‑tested allowances (children, primary residence costs, and specific energy/green deductions), because those reduce chargeable income before the brackets are applied.

In summary

With Cyprus income tax rates 2026 now active from 1 January 2026, you benefit from a higher tax‑free threshold, wider mid‑bands, and (when you qualify) household allowances that can reduce taxable income further—often translating into meaningful annual savings.

If you want to connect the income tax changes to the wider reform package, the “Cyprus Taxes 2026” guide provides a broader view of the measures that matter for individuals, investors, and property owners.

For questions about relocation and property plans in Cyprus, contact Sunshadow Investments Ltd at Artemidos Street, Number 3, 2nd Floor, 6025 Larnaca, Cyprus. Tel: +357 24 816246 | Fax: +357 24 816243 | Email: info@sunshadowinvest.com.

Disclaimer: This article is for general informational purposes only and should not be treated as tax or financial advice. You should confirm your position with your accountant or tax adviser.